John Rogers is an icon not only in finance, but also in education. Thirty years ago he founded Ariel Investments, changing finance in the process (he today is an advisor and on boards of many of the most prestigious companies, endowments and universities).

However, more importantly, as far as I am concerned, twenty years ago he founded the Ariel Foundation, “adopting” sixth grade students from the south side of Chicago with a promise to make college affordable for every student graduating from high school. The name later changed to the Ariel Education Initiative (AEI), and, jointly with Aon, Ariel publishes an annual retirement study focused on racial and gender analysis for retirement investing.

On the plus side, “401k Plans In Living Color” has immensely raised awareness in regard to gender and race inequalities when it comes to investing and access to quality resources. Still, a lot needs to be done beyond awareness, judging from the 2012 results.

Below are a few highlights – please share both the study and the findings widely within your teams, organizations, and beyond.

This study was conducted by AEI and Aon Hewitt, along with the Joint Center for Political and Economic Studies and The Raben Group. The findings are based on year-end 2010 information from 60 of the largest U.S. organizations across a variety of industries and sectors. The data, collected and analyzed by Aon Hewitt, represent 2.4 million employees.

While the first landmark study from 2009 looked at pre-crisis data, the 2012 show the impact of the crisis on retirement savings at large. One of the continuously disconcerting findings from the annual study is that African Americans and Hispanics lag behind in retirement assets compared to Asian Americans and whites.

Two courses of action to address the gap between race and gender are to implement policies and practices to reduce the withdrawal of funds prior to retirement and design plans to magnify the positive impact of auto-enrollment.

The 2007 Ariel/Aon Hewitt Study found that in each of the four essential areas of building account balances—establishing an account, contributing funds, allocating money appropriately, and preserving account balances by refraining from borrowing or prematurely withdrawing—disparities exist by race and ethnicity.

The cumulative effect of these disparities was that African-Americans and Hispanics have significantly lower average account balances in their 401k accounts, even across groups with similar salaries and age brackets.

The crisis left particularly African-American and Hispanic employees in financial distress, with 60% cashing out their retirement account entirely after losing their jobs. While the liquidity of the accounts is attractive as a short term life boat, the long term results are disastrous and the government should modify regulations that help bridge short term relief without sacrificing the future.

On the plus side, more employers now force workers to opt out of DC plans instead of asking them to enroll when they start, boosting participation rates especially among young and low salary employees.

Auto enrollment nearly eliminated that racial gap in participation rates!

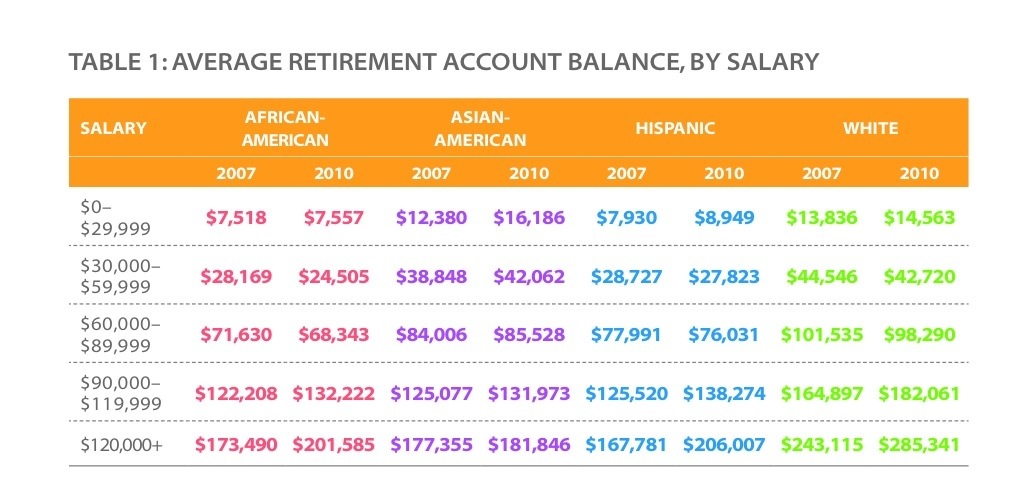

The most alarming data for me remains the average retirement account balance, especially for lower paid employees. Looking at the 30k-60k salary bracket, two sad statistics stand out.

– Account balances for Asian Americans and whites are over 60% higher than those of African Americans and Hispanics (42-43k vs. 25-28k)

– Account balances increased from 2007-2010 for Asian Americans and whites, but decreased for African Americans and Hispanics.

The two main reasons for those data points are auto-enrollment and preventing DC account withdrawals in times of hardship by offering other solutions.

Let’s put things bluntly: the location of your birth, the color of your skin, and your gender are the main determinants of your success in life.

Being born white, male and in a “developed” country still gives you the most significant head-start in life imaginable. Yes, an increasing number of minorities and women are successful today (as chronicled in the larger number of powerful women in business and politics today), but they are successful against all odds, not because it is a level playing field.

John Rogers and his AEI play an important role in leveling this playing field. Let’s do our part by sharing relevant data points and policies to raise awareness further.

Hopefully this century will change things ever so slightly.

I invite you to follow me on twitter @danenskat

(c) Enskat Associates 2012